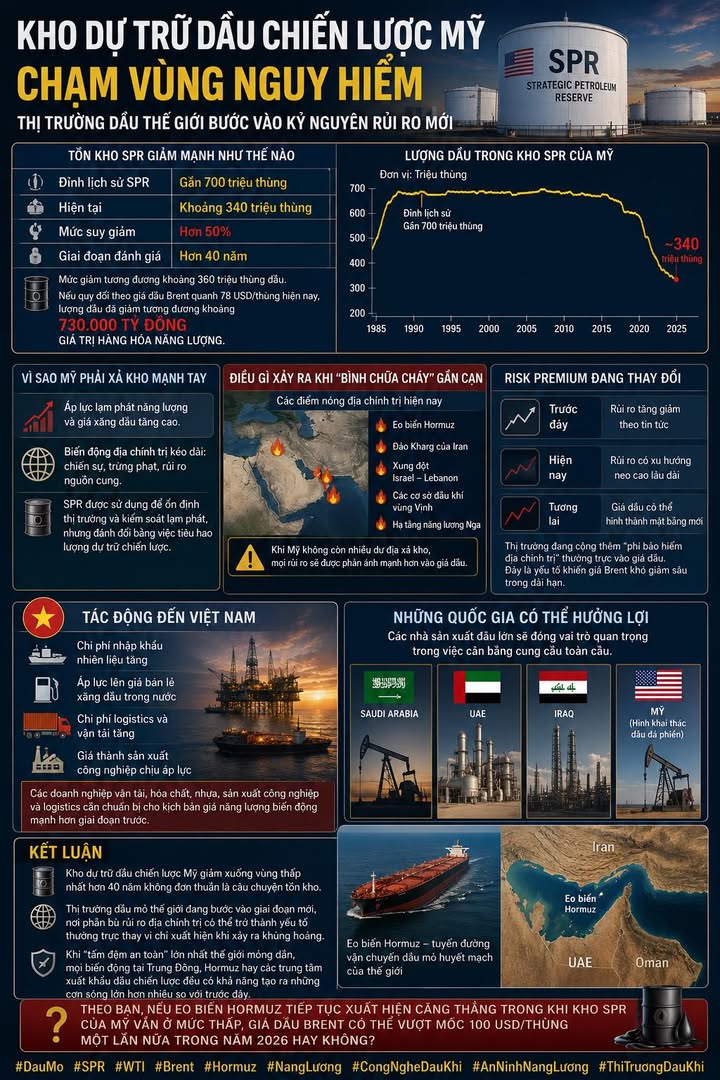

US Strategic Petroleum Reserve Reaches Critical Low, Global Oil Markets Enter New Era of Risk

The world's energy landscape is undergoing a fundamental shift as the United States Strategic Petroleum Reserve (SPR) has plummeted to approximately 340 million barrels, marking its lowest level in over 40 years. This development extends beyond mere inventory statistics, signaling a profound transformation in global oil pricing mechanisms and market dynamics.

Once considered the ultimate safeguard against global supply disruptions, the SPR's rapid depletion has raised critical questions about the world's capacity to respond to potential crises. If a new conflict were to erupt in the Middle East at this juncture, would the United States still possess adequate reserves to stabilize markets, or is the world on the brink of its most significant oil shock in decades?

The Current State of the Strategic Petroleum Reserve

The Strategic Petroleum Reserve, established in the aftermath of the 1973 oil crisis, has long served as America's energy security backbone. However, recent data reveals a dramatic reduction in this critical buffer:

| Metric | Current Level | Historical Peak | Reduction |

|---|---|---|---|

| SPR Inventory | ~340 million barrels | Nearly 700 million barrels | Over 50% |

| Equivalent Energy Value | ~$730 trillion (at $78/barrel) | N/A | N/A |

| Lowest Since | Over 40 years | N/A | N/A |

The reduction of approximately 360 million barrels represents a significant erosion of America's energy security cushion. At current Brent crude prices hovering around $78 per barrel, the value of depleted reserves exceeds $730 trillion in energy commodity terms.

Factors Driving the Aggressive SPR Drawdown

The unprecedented reduction in SPR levels stems primarily from two interconnected factors: persistent energy inflation and prolonged geopolitical tensions. As conflicts, sanctions, and threats in the Strait of Hormuz pushed oil prices to elevated levels, Washington utilized the SPR as a market stabilization tool.

This strategy achieved short-term success by alleviating pressure on fuel prices and helping control inflation. However, it came at the cost of significantly depleting reserves originally intended for emergency response scenarios. The Biden administration authorized multiple large-scale releases from the SPR, including:

- The largest release in US history - 180 million barrels in 2022

- Continued coordinated releases with other consuming nations

- Tactical releases responding to specific market disruptions

Implications of Diminished SPR Capacity

The concern surrounding the SPR's current state extends beyond the absolute quantity of remaining oil. The more significant issue lies in market psychology and the changing risk calculus for global energy markets.

When market participants recognize that the United States has limited capacity for large-scale strategic releases, geopolitical risks will be more fully and immediately reflected in oil prices. Current geopolitical hotspots that could trigger such market reactions include:

- The Strait of Hormuz - a critical chokepoint for global oil shipments

- Iran's Kharg Island - a vital oil export terminal

- The Israel-Lebanon conflict zone

- Oil facilities throughout the Persian Gulf region

- Russia's energy infrastructure amid ongoing sanctions

Any disruption at these critical nodes could now generate price volatility significantly more severe than during previous periods when the SPR maintained substantial reserves.

The Evolving Risk Premium in Oil Markets

A fundamental shift is occurring in how markets price geopolitical risk, with potentially lasting implications for global oil pricing:

| Historical Period | Current Period | Future Outlook |

|---|---|---|

| Risk premiums fluctuated based on specific news events | Risk premiums trending toward permanently elevated levels | Potential formation of a new price floor for oil |

In essence, markets are beginning to incorporate a permanent "geopolitical risk insurance premium" into oil pricing. This factor could prevent Brent crude from experiencing deep declines in the long term, even when physical supply conditions temporarily improve.

Impact on Vietnam and Import-Dependent Nations

As a significant energy importer, Vietnam will likely experience substantial consequences from these market shifts. A higher baseline for oil prices would translate into several economic challenges:

- Increased costs for imported fuel products

- Upward pressure on domestic retail fuel prices

- Rising logistics and transportation expenses

- Higher production costs for industrial manufacturers

Businesses across multiple sectors in Vietnam—including transportation, chemicals, plastics, manufacturing, and logistics—should prepare for scenarios involving more pronounced energy price volatility than previously experienced.

Potential Beneficiaries in the New Energy Landscape

Amid the SPR's decline and increasing geopolitical risks, certain nations and producers are positioned to gain greater influence in global energy markets:

- Saudi Arabia - As the world's largest oil exporter with substantial spare capacity

- United Arab Emirates - With significant production capacity and strategic storage facilities

- Iraq - Benefiting from expanding production infrastructure

- US shale producers - Potentially filling gaps in supply flexibility

Future Outlook and Scenarios

The reduction of the world's largest energy safety net to a 40-year low represents more than just an inventory story. It signals that global oil markets are entering a new phase where geopolitical risk premiums may become permanent features rather than crisis-driven fluctuations.

As the primary buffer against global supply disruptions diminishes, any volatility at strategic oil export centers—whether in the Middle East, the Strait of Hormuz, or other critical nodes—could generate market shocks significantly more severe than those previously observed.

Industry analysts are divided on whether this new normal will result in structurally higher oil prices or merely increased price volatility. What remains clear is that the era of abundant strategic reserves in consuming nations is drawing to a close, fundamentally altering the risk calculus for global energy markets.

Conclusion

The US Strategic Petroleum Reserve's descent to historically low levels marks a watershed moment in global energy markets. With the world's largest safety net thinning, market participants must recalibrate their risk assessments and develop new strategies for navigating an increasingly volatile energy landscape.

The implications extend far beyond American energy policy, affecting nations worldwide through altered price dynamics, changing supply relationships, and heightened sensitivity to geopolitical developments. As the global economy adapts to this new reality, one question looms large: If tensions in the Strait of Hormuz persist while US strategic reserves remain at minimal levels, could Brent crude once again surpass the $100 per barrel mark by 2026?